by wadminw on March 01, 2023

The column simply lists the discounts as with any other book of prime entry. Subsequently at the end of the accounting period, the business posts the total of the column to the general ledger discount allowed or received account as appropriate. The first three columns are the same as the single column cashbook and show the date, transaction description (Desc.), and ledger folio reference (LF).

To help you understand the recording procedure, a simple format is given below. In our example, the only other credit column featured in the deduction of higher ed expensess is for all other accounts. It is set up in the same way that the other column on the debit side is, except that the account title area is replaced by a “Ref.” column. As the example shows, a typical cash receipts journal consists of many columns.

As they are posted, the account numbers are placed in the post reference column. Keep in mind, the cash receipt process varies from business to business. You can tweak the above steps to better fit the workflow of your company. This ensures that the individual customers’ accounts are up to date and accurately reflect the balance owed at that date. The length of time you should keep a document depends on the action, expense, or event the document records. Generally, you must keep your records that support an item of income or deductions on a tax return until the period of limitations for that return runs out.

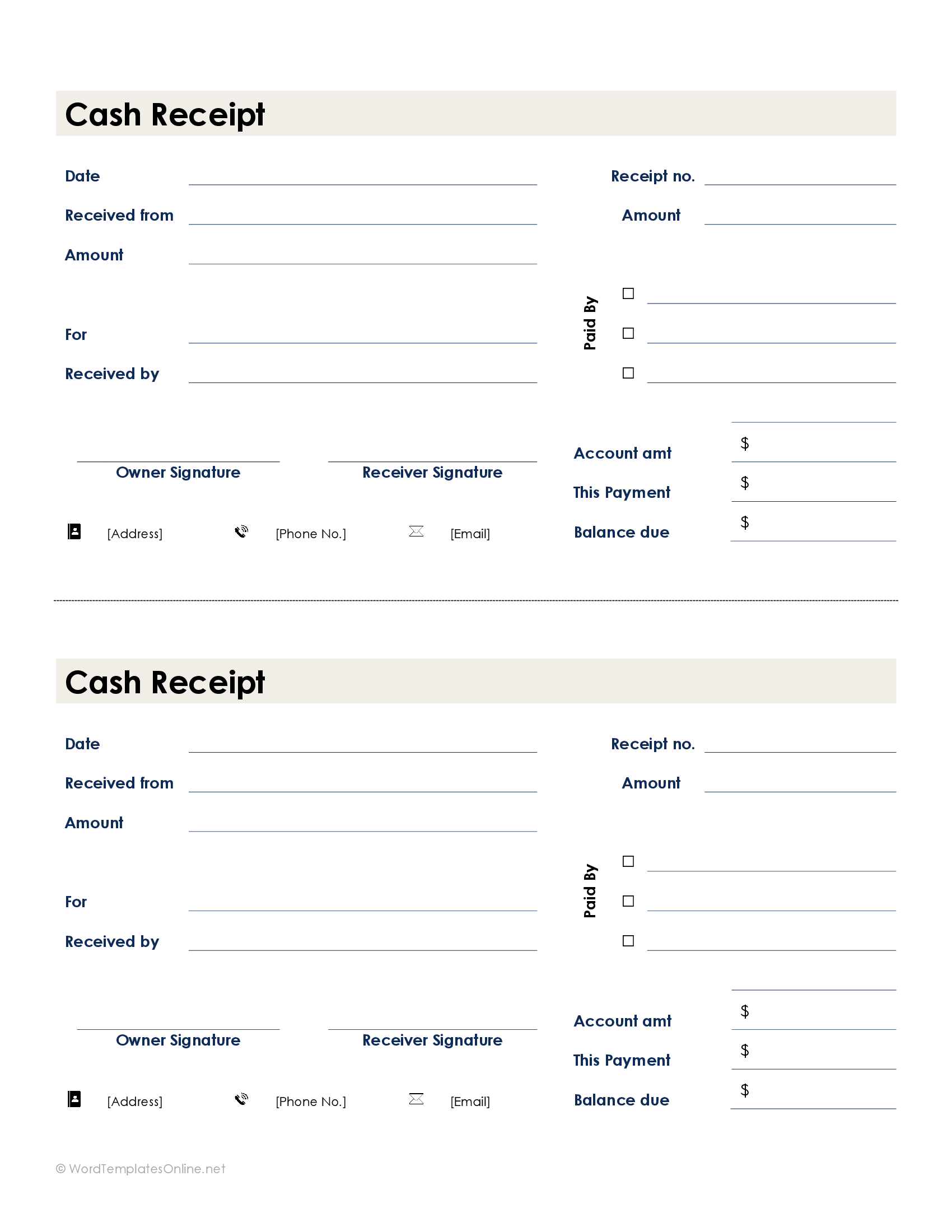

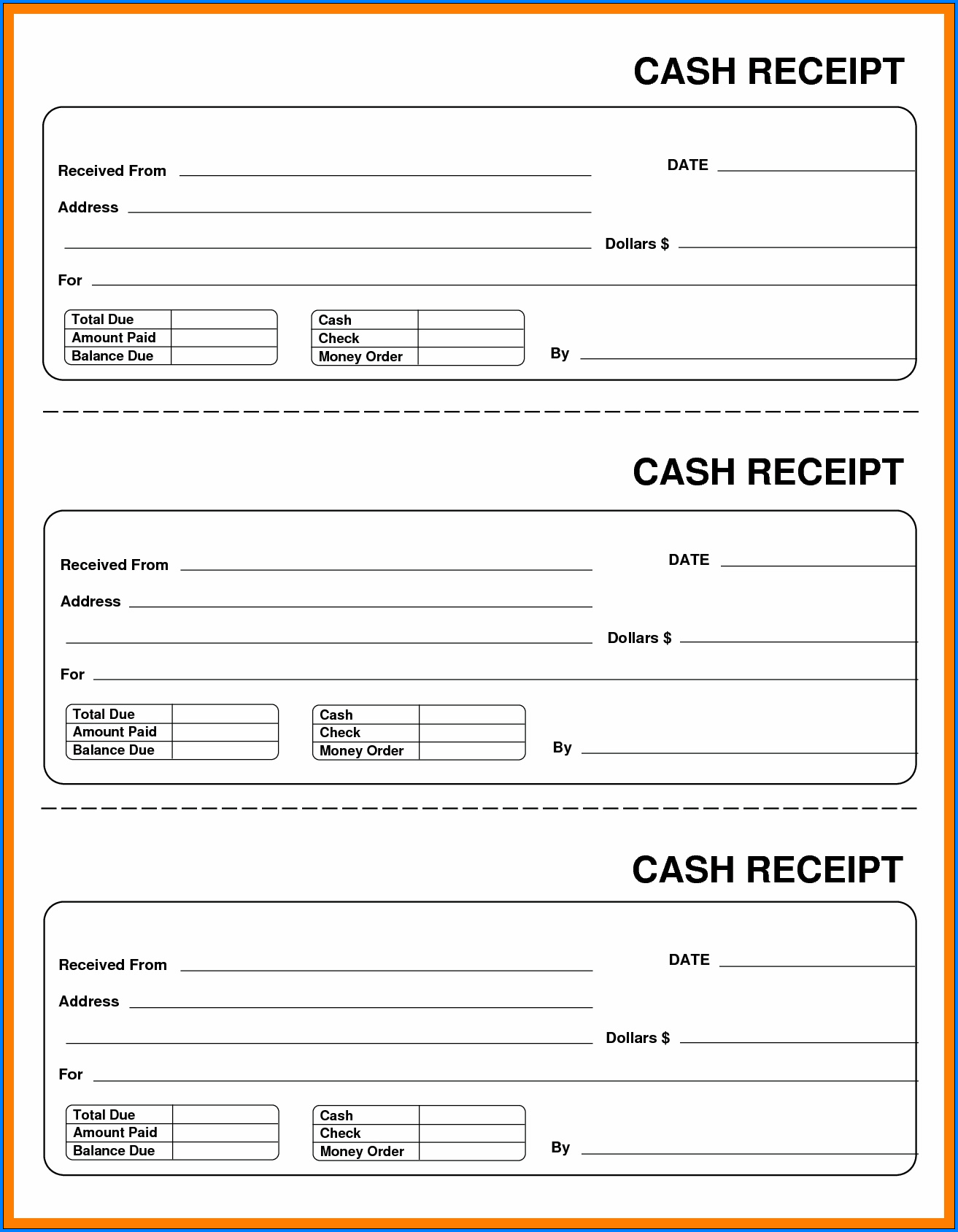

All additional cash sources, including bank interest, investment maturities, sales of non-inventory assets, sales of fixed assets, etc. After making credit sales to the consumer based on the advanced credit period, any money is subsequently collected. Irrespective of the number of sub-divisions, each page of the cash book can have a number of formats from single column to multi-column. The most popular formats are the two and three column formats as detailed below. Sales receipts typically include things like the customer’s name, date of sale, itemization of the products or services sold, price for each item, total sale amount, and sales tax (if applicable). Although these amounts are often posted at the end of the month, they could be posted more frequently.

If someone needs to investigate a specific cash receipt, they might begin at the general ledger and then move down to the cash receipts journal, from which they might obtain a reference to the specific receipt. The accountant would then use the reference number obtained from the journal to search through source materials and identify the specific receipt in question. If you plan on depositing cash payments, make sure your deposit slip amount matches your cash receipts journal. Store deposit receipts along with your other business receipts in case of any discrepancies. To keep your books accurate, you need to have a cash receipts procedure in place. Your cash receipts process will help you organize your total cash receipts, avoid accounting errors, and ensure you record transactions correctly.

A sales journal entry is a journal entry in thesales journalto record a credit sale of inventory. All of the cash sales of inventory are recorded in the cash receipts journal and all non-inventory sales are recorded in the general journal. All cash received by a business should be reported in the accounting records. In a cash receipts journal, a debit is posted to cash in the amount of money received. Therefore, a credit is needed for one or more other accounts that are affected by collecting cash.

In the cash receipts diary, all funds received from clients that fall under cash sales for goods and services are noted along with the counterparty’s name in the narration. The other side of the three column cash ledger would be headed ‘Credit’ and show an identical format with the three columns representing the monetary amounts of the cash payment, bank payment, and discounts received. For simplicity, the single cash ledger book diagram below shows only one side of the cashbook, in this case the left hand, receipts side (debit). The right hand, payments side (credit) would be identical in structure and format. GAAP attempts to standardize and regulate the definitions, assumptions, and methods used in accounting. There are a number of principles, but some of the most notable include the revenue recognitionprinciple, matching principle, materiality principle, and consistency principle.

The cash receipts journal would cover items like payments made by customers on an unpaid accounts receivable account or cash sales. Whereas the cash disbursement record would include items like payments made to vendors to lower accounts payable. The cash ledger book can act as both a journal and a ledger and comes in various formats. Most often these sales are made up of inventory sales or other merchandise sales. Notice that only credit sales of inventory and merchandise items are recorded in the sales journal.

In this example, the cash receipts journal records the cash inflows received by the business during June. Each transaction is documented with its date, description, invoice number (if applicable), and the amount received in the cash account column. The cash receipt is then allocated to the appropriate revenue account, such as sales or service fees, or applied against a customer’s accounts receivable balance if it’s a payment for an earlier invoice. A cash receipts journal is a specialized accounting journal used to record and track all cash inflows received by a business. This journal helps businesses organize and maintain a detailed record of cash transactions, providing an overview of the sources of cash and the amounts received during a specific period.

When a customer purchases inventory on credit, the sale isn’t directly recorded in the cash receipts journal because no cash has actually been collected. Instead, the accounts receivable account is debited and the sales account is credited. When the credit customer returns to pay off his account, cash is collected however. The cash receipts journal is typically totaled and summarized periodically (e.g., monthly) to update the general ledger accounts. The journal provides a convenient way to monitor and analyze cash inflows, helping businesses maintain accurate financial records, identify trends, and assess their cash management practices. Since no cash is received from credit sales transactions, they are not recorded in an accounting journal.

The cash receipts journal is used to record all transactions that result in the receipt of cash. The cash receipts diary also contains information on any additional loans that a person has taken out from banks or other financial institutions. Tax refunds for direct and indirect taxes, any fee or commission collected, or the maturity of an investment or insurance policy.